Why incorporate a business?

It’s a question many self-employed entrepreneurs eventually face, and while there’s no one-size-fits-all answer, understanding the potential benefits and risks can help you make the right decision.

Incorporating your business offers a number of strategic advantages. One of the biggest is limited liability, which legally separates your personal assets, like your home or savings, from business debts, lawsuits, or even bankruptcy. It’s a layer of protection that sole proprietorships simply don’t offer.

Corporations also come with valuable tax planning opportunities. You’ll have access to lower small business tax rates, the ability to defer income, and potentially split income with family members to reduce your overall tax burden. These strategies can result in significant savings over time.

Finally, incorporation can enhance your access to capital. Incorporated businesses often appear more credible to lenders and investors, making it easier to secure funding or attract investment for growth.

3 Key Benefits of Incorporating

- Limited Liability: Protects your personal assets from business-related risks.

- Tax Advantages: Benefit from lower corporate tax rates, income splitting, and tax deferral.

- Access to Capital: Easier to raise funds through loans or investors as an incorporated entity.

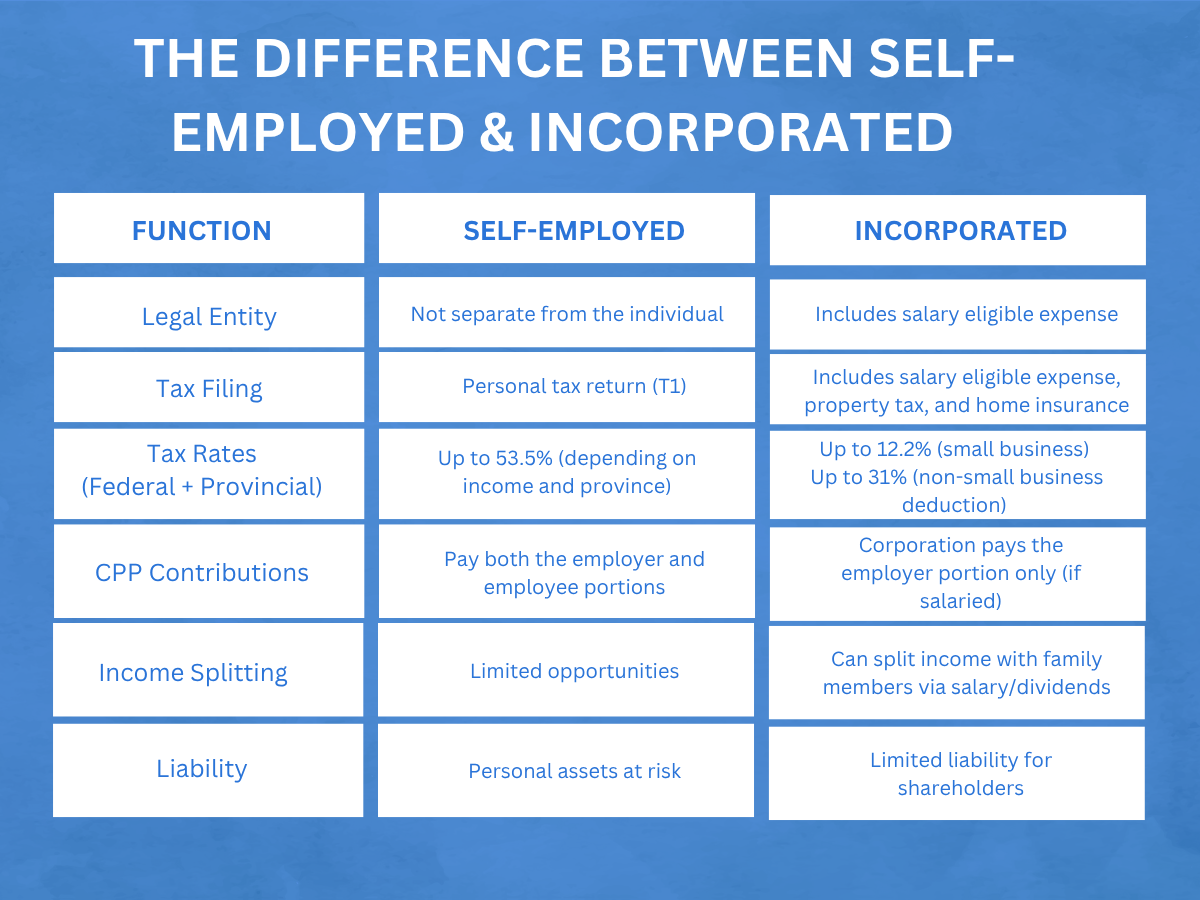

Self-Employed vs. Incorporated

To help you visualize the difference, we created a comparison of the legal, financial and compliance responsibilities between self-employment and incorporated businesses.

Advantages of Incorporating in Canada

Lower Corporate Tax Rates

One of the main financial advantages of incorporation is lower corporate tax rates, especially for small businesses. The small business deduction (SBD) is a program that provides lower federal and provincial tax rates for businesses that earn business income, with a limit of $500,000 or less. The normal federal corporate tax rate is 15%, with the SBD deduction its 9%. While the tax rates vary based on low and high-income-generating businesses, each province assigns different tax rates. However, in comparison to the personal tax rate, it is much lower.

Income Deferral and Tax Planning

If your business earns more than you need personally, you can leave profits in the corporation and defer tax until funds are withdrawn. This enables long-term tax deferral and investment growth within the corporation with limited tax liabilities.

Income Splitting

With proper structuring, you can pay dividends or salaries to adult family members who are shareholders or employees, reducing your overall tax burden. The business owner can split his income with a spouse or adult child who has a lower tax rate, thus potentially saving thousands on taxes.

It’s important to note that Canada introduced TOSI, which restricts business owners on who is eligible for income splitting.

These exceptions exist for the following:

- Spouses aged 65+

- Adult children who work 20+ hours per week in the business

- Reasonable return on capital contributions

Limited Liability Protection

When incorporated, your personal and business assets are considered separate. This limits your liability in situations of bankruptcy, lawsuits, or creditors which fall under the corporation.

Limited liability is not always absolute, as owners or directors can be personally liable. These situations are the following:

- Personal guarantees with a bank loan or lease

- Unpaid taxes, such as unremitted GST/HST or payroll deductions

- Fraud or negligence where the court pierces the corporate veil, ensuring the individual is personally liable

- Environmental and labour law violations that were breached can force directors and owners to be personally liable.

Increased Business Credibility

One significant advantage of being incorporated is access to funding. Lenders and investors are more willing to provide capital to support your growth due to the better financial transparency of incorporated businesses. Depending on your size and industry, it opens new opportunities with larger enterprises that exclusively work with incorporated entities with more favourable payment or credit terms.

You Wanna Be Incorporated or Stay Self-Employed?

Making this transition is not a simple business decision. Connect with a CPA accountant for expert financial guidance.

Disadvantages of Incorporating a Business

Higher Administrative Costs

Incorporating brings added costs that require the setup fee, which typically costs between $200-$400, depending on the complexity of your business. With increased legal, financial, and compliance responsibilities, it requires annual filing, financial reporting (T2), and payroll or employee remittance for CPP, EI, and income tax.

Ongoing Compliance

Incorporated businesses have ongoing obligations which are designed to provide financial transparency and accountability to governments, shareholders, and employees.

These compliance obligations ensure you are meeting the requirements of CRA with the following:

- T2 Corporate tax returns

- Payroll remittances

- GST/HST Filing

- T4/T5 slips

Double Taxation on Withdrawals

For businesses, profit is taxed at the corporate tax rate. However, when withdrawing money via salary or dividends, it can be taxed again at the personal level. Depending on the situation, speak with your trusted accountant to discuss new opportunities to minimize double taxation.

Limited Tax Loss Utilization

Unlike self-employment, when your business incurs a loss, you can offset your taxable personal income. Once incorporated, individuals will not be able to offset their income as corporations are a separate entity, which stays within the company.

When Should I Incorporate My Business

If you are self-employed and still unsure about whether you should incorporate your business. Here are a few questions: We ask our clients to help assess their situation in determining a plan:

- Do you earn more income than what you actually spend?

- Remember, for corporations, owners get taxed twice. So, if you are withdrawing more money than you are spending, it would be greatly beneficial to retain your income or defer your taxes.

- What are the liabilities in your business?

- Your liability risk depends on your industry. In high-risk fields like the trades, where accidents with heavy machinery are more likely, incorporating can protect your personal assets by legally separating them from business risks.

- Do you plan to hire employees?

- If your business is growing to a capacity where you need workers to help maintain and grow, incorporating will make payroll remittance easier to manage.

How to incorporate my business

- Choose Federal or Provincial Incorporation

- Federal incorporation offers better protection if you sell across Canada, but requires you to register both federally and in each province you sell in.

- Provincial incorporation is sufficient if you plan to operate in one province, which is common for local businesses.

- Name Your Corporation

- You can choose a named corporation or go with a numbered corporation

- Prepare & File Document of Incorporation

- This legal document includes information about:

- Corporate name or number

- Registered office address

- Names and addresses of directors

- Share structure

- Incorporator information

- Articles of incorporation

- This legal document includes information about:

- Register for CRA Accounts

- All businesses will need to register for a business number, GST/HST, payroll, and, if applicable, import/export accounts.

- Establish a Corporate Bank Account

- All business income and expenses should flow through a separate corporate account for bookkeeping and tax purposes, which will help with filing your year-end.

- Set Up Shareholder Agreements and Minute Books

- Proper documentation of your company, known as the minute book that helps resolve disputes and ensures CRA compliance.

- Work with a Professional Accountant and Lawyer

- Incorporation requires expert setup for tax efficiency and legal protection. Our accountants at Advanced Tax will help guide you through the process that reflects your goals.

Let us help you Incorporate Your Business

Any self-employed business owner can incorporate their business. However, it’s important to assess the risk and benefit ratio to be incorporated. While it possesses many advantages, from tax savings, funding opportunities, and unlimited liability, does the cost and increased responsibilities improve your bottom line? That’s why with Advanced Tax, we help guide you through this critical decision to ensure that your decision makes sense and aligns with your financial goal. Get in touch with an expert accountant.s, consult a tax professional to ensure you’re getting the full benefit. the work-from-home tax credit.